The 60-20-20 Rule: A Simple Budget Strategy for Working Professionals

If you’ve ever felt overwhelmed by complicated budgeting spreadsheets or guilty about spending money on things you enjoy, you’re not alone. Many working professionals struggle to find a budgeting method that’s both effective and realistic. Enter the 60-20-20 rule—a straightforward budgeting strategy that helps you manage your finances without making you feel like you’re living on a shoestring.

Think of the 60-20-20 rule as your financial GPS. It won’t micromanage every turn you make, but it’ll keep you headed in the right direction. Whether you’re just starting your career or looking to simplify your financial life, this budgeting method might be exactly what you need.

What is the 60-20-20 Rule?

The 60-20-20 budgeting rule is a simple money management strategy that divides your monthly net income (that’s your take-home pay after taxes) into three clear categories:

- 60% for Living Expenses: This covers your essential needs—rent or mortgage, utilities, groceries, insurance premiums, transportation costs, minimum debt payments, and other necessities you can’t live without.

- 20% for Savings: This portion goes toward building your financial future. Think emergency funds, retirement accounts like your 401(k) or IRA, health savings accounts, education funds, or saving for a down payment on a house.

- 20% for Non-Necessities: This is your guilt-free spending money for the things that make life enjoyable—dining out, streaming subscriptions, shopping, hobbies, travel, concerts, and entertainment.

The beauty of this personal finance strategy is that it’s based on percentages, not fixed dollar amounts. This means it scales with your income and adapts to your unique financial situation.

Why the 60-20-20 Budget Works

What makes the 60-20-20 rule so appealing to working professionals? Let me break it down:

Flexibility is Built In: Unlike rigid budgeting systems that track every penny, the 60-20-20 method gives you freedom within each category. As long as your living expenses stay under 60%, you can decide exactly how to allocate those funds based on your priorities.

It’s Remarkably Simple: You don’t need fancy budgeting apps or complicated formulas. Just three percentages and three categories. Anyone can understand and implement this budget framework in under an hour.

Saving Becomes Automatic: By dedicating 20% to savings right off the bat, you’re practicing the “pay yourself first” principle that financial advisors love. Your savings aren’t what’s leftover—they’re a built-in priority.

Balance Between Responsibility and Enjoyment: The 60-20-20 rule acknowledges that you’re human. You work hard, and you deserve to enjoy your money. That 20% for wants means you can grab coffee with friends or book that weekend getaway without derailing your financial goals.

How to Implement the 60-20-20 Rule

Ready to put the 60-20-20 budget plan into action? Here’s your step-by-step guide:

Step 1: Calculate Your Net Monthly Income

Start by figuring out exactly how much money hits your bank account each month after taxes, health insurance, and other deductions. If you’re paid biweekly, multiply one paycheck by 2.17 to get your monthly average. Include any side hustle income or other regular earnings.

Step 2: Do the Math

Once you know your net income, multiply it by 0.60, 0.20, and 0.20 to determine your three spending limits. For example, with a $5,000 monthly net income, you’d allocate $3,000 for living expenses, $1,000 for savings, and $1,000 for non-essentials.

Step 3: Categorize Your Current Expenses

Pull up your last three months of bank and credit card statements. List every expense and sort them into your three buckets. Be honest about what’s truly essential versus what’s a want. That daily latte? Probably belongs in the wants category.

Step 4: Make Adjustments

If your current spending doesn’t align with the 60-20-20 breakdown, identify where you can trim. Maybe you can meal prep more often, find a cheaper insurance provider, or cut back on subscription services you barely use. Small changes add up quickly.

Real-World Example: The 60-20-20 Rule in Action

Let’s look at how Sarah, a 32-year-old marketing manager, uses the 60-20-20 budgeting method:

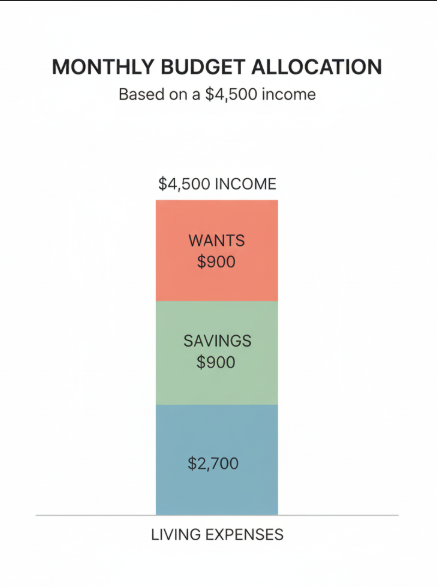

Sarah’s Monthly Net Income: $4,500

Living Expenses (60% = $2,700)

- Rent: $1,400

- Utilities: $150

- Groceries: $400

- Car payment: $300

- Car insurance: $120

- Gas: $150

- Phone bill: $80

- Student loan minimum payment: $100

- Total: $2,700

Savings (20% = $900)

- Emergency fund: $400

- 401(k) contribution: $350

- Vacation fund: $150

- Total: $900

Non-Necessities (20% = $900)

- Dining out: $300

- Entertainment: $150

- Gym membership: $80

- Shopping: $250

- Miscellaneous fun: $120

- Total: $900

When Sarah first started tracking her spending, she was spending $1,200 on wants and only saving $600 monthly. By implementing the 60-20-20 rule, she cut back on impulse purchases and takeout orders. Six months later, she has $2,400 in her emergency fund and doesn’t feel deprived because she still budgets for the experiences she values.

Who Should Use This Budget Method?

The 60-20-20 financial plan works particularly well for:

Budgeting Beginners: If you’ve never followed a budget before, this system won’t overwhelm you with complexity. It’s a perfect starting point for developing financial awareness.

People Who Value Flexibility: Maybe your expenses fluctuate from month to month, or you like having control over how you spend within broad categories. The 60-20-20 rule accommodates that.

Moderate Earners: If you make enough to cover your basic needs with room left over, this budget strikes a nice balance between saving and spending.

Those Who’ve Failed at Restrictive Budgets: If tracking every coffee purchase makes you want to give up entirely, this higher-level approach might be your solution.

When the 60-20-20 Rule Might Not Be Right for You

While the 60-20-20 rule works for many people, it’s not universally perfect. Consider alternative budgeting strategies if:

You’re Living in a High Cost-of-Living Area: If you’re in San Francisco, New York, or another expensive city, your essential expenses might easily exceed 60% of your income. You might need a 70-20-10 or 50-30-20 split instead.

You Have Significant Debt: If you’re carrying high-interest credit card debt or substantial loans, you should probably allocate more than 20% toward aggressive debt repayment rather than wants.

Your Income is Very Low: When you’re struggling to make ends meet, 60% might not be enough for essentials, leaving little room for the 20% savings goal.

You’re an Aggressive Saver: If you’re working toward early retirement or have ambitious financial goals, you might prefer a method like the 60-30-10 rule (60% savings, 30% needs, 10% wants).

Tips for Making Your 60-20-20 Budget Successful

Want to maximize your results with the 60-20-20 money management system? Follow these pro tips:

Set Specific Financial Goals: Saving 20% feels more motivating when you know exactly what you’re saving for. Whether it’s a three-month emergency fund, a European vacation, or early retirement, name your goals.

Average Out Variable Expenses: Your grocery bill might fluctuate, and your utility costs change with the seasons. Look at three to six months of data to calculate realistic averages for your 60% allocation.

Automate Everything You Can: Set up automatic transfers to savings accounts and automatic payments for bills. When the money moves without your involvement, you won’t be tempted to spend it.

Review and Adjust Regularly: Life changes. You get a raise, move to a new city, get married, or have a baby. Revisit your budget quarterly to ensure it still reflects your reality.

Track Your Progress: Even though this isn’t a penny-pinching budget, checking in weekly or monthly helps you stay on track. A quick 10-minute review of your spending keeps you accountable.

Be Patient With Yourself: If you overspend in one category during your first month, that’s okay. Budget planning is a skill that improves with practice.

Alternative Budgeting Methods to Consider

If the 60-20-20 rule doesn’t quite fit your situation, explore these alternative budget strategies:

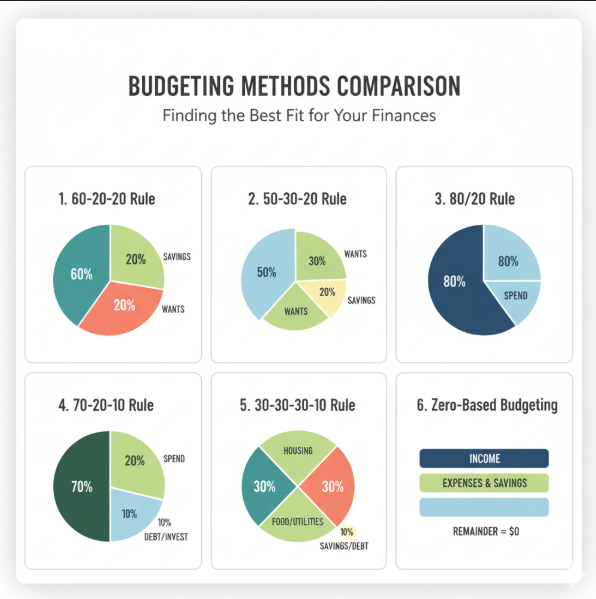

- 50-30-20 Rule: Allocate 50% to needs, 30% to wants, and 20% to savings. This is ideal if your essential expenses are lower or if you want more discretionary spending.

- Zero-Based Budget: Assign every single dollar a job until you have zero left to allocate. This detailed approach works well for people who love structure.

- 70-20-10 Rule: Split your income into 70% for spending, 20% for saving, and 10% for giving or extra debt payments. Great for those who prioritize charitable giving.

- 80/20 Rule: The simplest of all—80% for combined needs and wants, 20% for savings. Perfect for absolute beginners who find even three categories overwhelming.

- 30-30-30-10 Rule: Designate 30% for housing, 30% for other necessities, 30% for savings and debt, and 10% for wants. This works well if housing costs are your biggest challenge.

Each budgeting method has its strengths. The best budget is the one you’ll actually stick with consistently.

Final Thoughts

The 60-20-20 rule isn’t about perfection—it’s about progress. It gives you a framework to make intentional decisions with your money while maintaining the flexibility to live your life. You’re not depriving yourself or obsessing over every transaction. You’re simply being more mindful about where your hard-earned money goes.

Whether you’re drowning in receipts, living paycheque to paycheque, or just looking for a better system, this budgeting approach offers a realistic path forward. It respects that you have bills to pay, goals to reach, and a life to enjoy—all at the same time.

Remember, personal finance is exactly that: personal. The 60-20-20 rule is a starting point, not a rigid prescription. Adapt it to your circumstances, combine it with other financial strategies, and adjust as your life evolves.