What Happens If You Buy a Home at the Top of the Market?

A Smart Buyer’s Guide to Risk, Recession, and Recovery

Imagine this: you finally close on your dream home in a hot market — bidding wars, waived contingencies, offers over asking price. Then six months later, a housing market recession hits. Your neighbor’s identical house just sold for $40,000 less than what you paid. Sound like a nightmare? It doesn’t have to be — if you prepared for it.

The decision to buy a home at the top of the market is one of the most stressful financial moves an American homebuyer can make. But with the right mindset, a sound strategy, and a clear understanding of mortgage affordability, you can survive — and even thrive — through a downturn.

Table of Contents

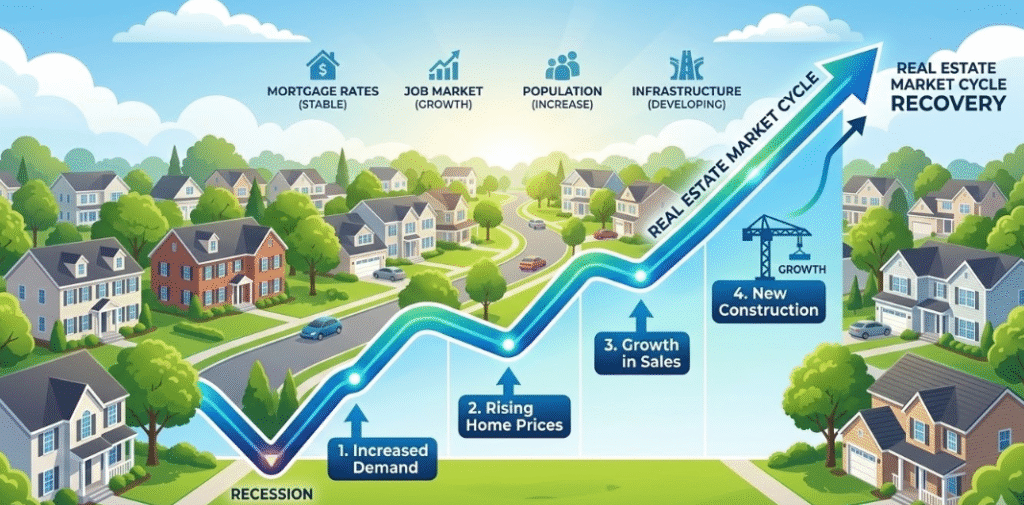

Understanding the Real Estate Market Cycle

Before diving into survival tactics, it helps to understand how the real estate market cycle works. Real estate doesn’t crash overnight. It moves in four broad phases: Recovery, Expansion, Hypersupply, and Recession. Each phase can last years.

Here’s what each phase generally looks like in plain English:

- Recovery: Prices are flat or slowly climbing. Inventory is high, buyers have negotiating power.

- Expansion: Demand is rising, new construction picks up, prices climb steadily.

- Hypersupply: Builders overshoot demand. Too many homes hit the market. Price growth slows.

- Recession: Demand drops sharply. Prices fall. Foreclosures rise. This is real estate boom and bust at its most painful.

Historically, the bust phase lasts between one to three years before a price floor forms. In 2022–2024, rising mortgage rates from Fed interest rate cuts reversals created a standoff between buyers and sellers — a rare market freeze. That freeze is now thawing, and housing market crash fears are re-emerging in some regions.

The Core Home Buying Risk: What Could Go Wrong?

When you buy a home at the top of the market, the biggest home buying risk isn’t just a drop in paper value — it’s what happens if your income disappears at the same time.

Consider these real scenarios:

- A tech layoff sweeps through San Francisco Bay Area — your employer announces cuts.

- The S&P 500 performance tanks 20%, wiping out your stock portfolio.

- Your adjustable-rate mortgage resets, and your monthly payment spikes.

- A medical emergency drains your emergency fund.

In each case, the question isn’t just “Can I afford this house?” but “Can I keep affording it under pressure?” This is why mortgage affordability must be evaluated not just at closing — but across worst-case scenarios.

The 30/30/3 Rule: Your Built-In Safety Net

Financial experts recommend following the 30/30/3 rule when buying a home:

- Spend no more than 30% of your gross income on monthly housing costs.

- Have at least 30% of the home’s value in cash (20% down payment + 10% reserve).

- The home price should be no more than 3x your annual gross income.

Sticking to this rule dramatically reduces your home buying risk. It also protects your loan-to-value ratio, which matters enormously if you ever need to mortgage refinance. Most lenders won’t refinance if your LTV exceeds 80%, so maintaining equity is critical.

What Happens Emotionally and Financially After Buying at the Peak

If the market turns after your purchase, here’s what typically unfolds:

Phase 1 — Denial (Months 1–12)

This is known as buyer denial. You’ll rationalize your purchase — better layout, better neighborhood, better school district. You’ll tell yourself the market will bounce back. And maybe it will.

Phase 2 — Acceptance (Months 12–24)

You start comparing your purchase price to nearby sales. You realize you might have overpaid. This is normal. The key is not to panic — and not to make emotional decisions.

Phase 3 — Worst-Case Scenario Planning

Worst-case scenario planning becomes necessary. You ask: How long can I make payments if I lose my job? Am I heading toward an underwater mortgage? Should I look into foreclosure / short sale options? Know your state’s non-recourse states laws — in non-recourse states, the lender cannot come after your other assets if you walk away.

Phase 4 — Budget Cutting in Recession

Budget cutting in recession mode kicks in. You slash subscriptions, eat at home, defer vacations. This is actually healthy financial behavior — forced frugality often reveals just how much fat was in your spending.

Budgeting With No Money: How to Start From Zero

Here’s a truth most real estate articles skip: sometimes buying a home stretches you so thin that you’re essentially budgeting with no money. Whether it’s a depleted down payment, unexpected repairs, or a job loss — you may find yourself starting from financial scratch after closing.

Here’s a practical 8-step survival framework:

- Full Financial Awareness — List every income source and every single expense, no matter how small. Ignorance is the enemy.

- Categorize Ruthlessly — Split expenses into Needs (mortgage, utilities, groceries), Obligations (minimum debt payments), and Wants (everything else).

- Enter Survival Mode — Cut every non-essential: streaming services, dining out, gym memberships, subscriptions.

- Build a Bare-Bones Budget — Focus only on essentials and minimum payments. This is your comeback budget.

- Track Every Dollar — Regain control and clarity. If you know where every dollar goes, you’re no longer a victim of your finances.

- Increase Income — Side gigs, freelancing, selling unused items — all of it counts. Every extra dollar should have a job.

- Track Small Wins — Paid off one credit card? Saved $200 this month? Celebrate it. Motivation is built on momentum, not perfection.

- Remember: This Is Temporary — Your financial situation right now is not your permanent story. Budgeting is your first step forward.

The discipline you build budgeting with no money is exactly the same discipline that will protect you during a housing market recession. They’re two sides of the same coin.

Alternatives to Going All-In: Real Estate Without a Mortgage

Not ready to commit to a full mortgage? You still have options to build real estate wealth while managing home buying risk:

- REITs / real estate ETFs: Publicly traded. No leverage required. Liquid.

- Real estate crowdfunding: Platforms allow you to invest in diversified portfolios with small amounts.

- Private real estate funds: For accredited investors. Higher minimums, but strong diversification.

- Dollar-cost averaging: Invest smaller amounts consistently rather than a lump sum at a market peak.

- Heartland real estate: Coastal vs. heartland markets — Sunbelt real estate and Midwest cities are often in earlier phases of the real estate market cycle with stronger yield potential.

These strategies are especially valuable if you believe we’re nearing the top of a real estate boom and bust cycle in expensive coastal markets like the San Francisco Bay Area or NYC.

Can You Refinance If Home Value Drops?

This is one of the most common long-tail questions homeowners ask: can you refinance if home value drops? The short answer: it depends on your equity.

Most lenders require a loan-to-value ratio of 80% or lower to qualify for the best rates. If your home drops in value and you dip below 20% equity, your refinancing options shrink. This is why acting early — before your equity erodes — is critical.

Pro tip: If you see the market softening, initiate a mortgage refinance inquiry before you lose your job. Banks will not refinance unemployed applicants, no matter how strong your credit.

The Bottom Line: How to Survive Buying a Home at the Peak

If you’ve already bought — or you’re about to — here are the non-negotiables:

- Follow the 30/30/3 rule at purchase.

- Keep at least 3–6 months of mortgage payments in a liquid emergency fund.

- Understand your loan-to-value ratio and protect your equity.

- Be ready to enter budget cutting in recession mode if needed.

- Know your state’s rules on foreclosure / short sale and non-recourse states.

- Consider real estate crowdfunding, REITs / real estate ETFs, or private real estate funds for diversified, lower-risk exposure.

Buying at the top of the market is not a death sentence. What happens if you buy a house during a recession depends almost entirely on your preparation. If your finances are solid, your budget is lean, and your income is diversified — you will get through it. The real estate market cycle always turns. And history shows that those who hold on through the downturn almost always come out ahead.

| Key Takeaway Your current financial situation is temporary. Whether you’re budgeting with no money after a big down payment or navigating a housing market recession, the principles are the same: awareness, discipline, and a long-term plan. Real estate rewards those who stay the course. |

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Always consult a licensed financial advisor or real estate professional before making major investment decisions.